Estimated reading time: 5 minutes

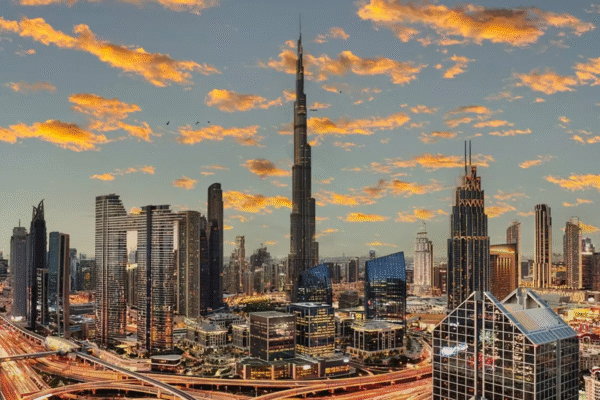

Dubai’s luxury real estate market continues to command record prices, with Jumeirah Bay Island now ranked as the most expensive neighborhood in the city. Research published by Driven Properties and Forbes shows values on the island averaging Dh13,068 per square foot, far outpacing other high-end areas and underlining the city’s status as a global hub for ultra-wealthy buyers.

The surge reflects a broader shift in Dubai’s property sector, where exclusivity, location, and supply constraints have created some of the most expensive homes in the world. Jumeirah Second and Umm Al Sheif follow as the next most costly neighborhoods, each recording average prices of more than Dh7,500 per square foot. These figures highlight not only demand for villas and low-density seaside communities but also the resilience of Dubai’s top-tier housing market.

Luxury enclaves such as La Mer, Bluewaters Island, Palm Jumeirah, and Emirates Hills have maintained their appeal. Analysts point to a mix of waterfront access, privacy, and restricted availability as the driving factors. With global buyers increasingly looking for safe havens for both capital preservation and lifestyle, Dubai has successfully positioned itself alongside markets such as London, New York, and Singapore.

The city’s transformation into a luxury destination has coincided with parallel momentum in mid-market and affordable segments. Jumeirah Village Circle, for instance, has seen strong transaction volumes, illustrating that while luxury neighborhoods dominate headlines, demand across the board is sustaining overall market depth.

Data shows that Dubai’s residential market has strengthened considerably over the past four years. Average ready property prices rose from Dh1,002 per square foot in the first quarter of 2021 to Dh1,642 by the second quarter of 2025, marking a 64 percent increase. Analysts say this growth is notable not only for its scale but for its consistency, reflecting confidence from both end-users and investors.

The convergence of villa and apartment prices is particularly striking. Villas moved from Dh1,010 per square foot in early 2021 to Dh1,903 in early 2025, while apartments climbed from Dh1,036 to Dh1,763 over the same period. By the second quarter of 2025, both hovered near Dh1,903–1,904, suggesting balanced demand between family-oriented homes and compact residences. Experts argue that this alignment points to a more mature and diversified buyer base.

Transaction volumes reinforce the trend. Quarterly sales rose from just over 10,000 in early 2021 to more than 51,000 in the second quarter of this year. Off-plan sales in particular have surged, climbing from 4,219 units in Q1 2021 to 36,184 in Q2 2025. That means more than 70 percent of current deals are driven by developer launches, signaling a developer-led market. Ready property sales, while slower, still rose steadily to 15,170 units in the latest quarter, indicating ongoing demand for completed homes that offer immediate rental income and reduced risk.

Price growth in the off-plan sector has been equally striking. From Dh1,354 per square foot in Q1 2021, average prices reached Dh1,866 in Q2 2025, a jump of 38 percent. Apartments, in particular, have led the rise, reaching Dh2,288 per square foot, supported by demand for branded residences and lifestyle-driven communities. Villas in off-plan projects more than doubled in value, increasing from Dh834 to Dh1,682 per square foot, highlighting preferences for spacious, family-friendly living in integrated developments.

Market watchers say the flattening of growth curves since 2024 suggests a stabilizing cycle. With prices rising steadily rather than sharply, fundamentals rather than speculation appear to be driving activity. Developers are focusing on project quality, location, and brand credibility, while buyers are showing more strategic preferences.

Population growth and policy support add further strength. Dubai’s population, now over four million, is growing by roughly five to six percent annually. Pro-residency initiatives such as the Golden Visa and remote work permits are boosting confidence among international buyers. At the same time, local end-users are becoming more prominent, encouraged by flexible payment plans and rising rental costs that make ownership a competitive alternative.

The Dubai luxury real estate market is also benefiting from an influx of ultra-high-net-worth individuals. According to Henley & Partners, the city is now home to more than 80,000 millionaires, a number expected to climb as geopolitical and economic uncertainty continues to push global wealth into stable havens. Villas on Jumeirah Bay, Palm Jumeirah mansions, and penthouses on Bluewaters have become symbolic purchases for this demographic.

Analysts note that while record prices attract headlines, Dubai’s strength lies in its layered structure. The city simultaneously accommodates the ultra-luxury segment and the mid-market, allowing it to absorb supply more effectively. This balance is expected to be critical as more than 150,000 new units are delivered between 2025 and 2027.

For now, momentum remains strong. The narrowing price gap between apartments and villas suggests confidence across asset classes, while steady sales volumes demonstrate broad-based participation. As affordability in some premium areas narrows, end-users are shifting into emerging districts where value and lifestyle align.

The long-term outlook appears stable. With sustained demand from global wealth, growing population pressure, and steady developer activity, Dubai seems positioned to maintain its place as one of the world’s leading real estate markets. The resilience of Jumeirah Bay Island at the top end of pricing underscores this narrative, while the breadth of activity across mid-tier neighborhoods highlights a city that caters to diverse needs.

Its exclusivity, prime location, and limited villa plots have pushed average prices to Dh13,068 per square foot.

By mid-2025, both asset classes averaged around Dh1,903 per square foot, showing balanced demand.

Flexible payment plans, branded residences, and lifestyle communities have driven off-plan sales to more than 70% of total transactions.

With annual growth of 5–6% and more than four million residents, population pressure is a major driver of housing demand.

Analysts suggest steady growth, strategic buyers, and strong fundamentals indicate a more stable, resilient cycle.